Government and lender mortgage modification programs have resulted in little success at helping people permanently modify home loans who are facing foreclosure. Many debtors tell of lenders losing paperwork, not responding to inquiries, misunderstanding modification program requirements and offering modifications that do little to respond to their needs. There are options available to people facing foreclosure. Some debtors have successfully challenged a foreclosure based on improper servicing by the lender. Others have used Chapter 13 bankruptcy to cure mortgage loanRead more

Too Proud to File Bankruptcy? Think Again.

Most people in debt are, at least initially, resistant to filing bankruptcy. Filing chapter 7 or chapter 13 is sometimes viewed as taking the easy way out, or looked at as a good way to ruin credit scores, or as a moral failing to be avoided. These feelings, combined with the inability to pay debts, result in a great deal of stress. The fact is that people do have pride, and no one wants to file bankruptcy if it canRead more

Damages from creditors could put money in your pocket!

Some of our clients have the cost of their bankruptcy case paid for with damages they receive from their creditors. There are several situations within bankruptcy filing that may result in compensation for you. Compensation from creditors may include: Stay violation: creditors attempting to collect a debt after the bankruptcy is filed Discharge violation: creditors attempting to collect a debt after the bankruptcy is complete Debt Collection Violations: creditors harassing, threatening, falsely representing themselves, contacting 3rd parties regarding your debtsRead more

Sub-Prime Mortgages Reappear Under New Name

Do you remember this dirty word from not so long ago: “sub-prime?” In hindsight, its usage and manipulation by lending institutions catapulted our economy into the toilet…a move we’re still trying to recover from. With investors holding billions of dollars in properties they need to sell, two of the largest financial institutions, Wells Fargo and Citadel Servicing Corp., are back in the sub-prime game. Only this time they’re operating under the guise of a “Second Chance Purchase Program.” What DoesRead more

Credit Report Mistakes

The Attorney General of Mississippi has filed a lawsuit against Experian, which, along with Transunion and Equifax, make up the three largest credit reporting companies. These companies collect information about consumers and then sell it back to lenders, insurance companies and others. What Was The Problem? The problem is that these reports on consumers are frequently full of mistakes and misinformation. According to investigators with the Mississippi Attorney General’s office, Experian: mixed up reports of consumers with the same orRead more

Is This Debt Yours?

According to the Federal Reserve, one in seven Americans is being contacted by a debt collector. This is up from one in twelve just ten years ago. Where Is My Debt? With 4,500 debt collection agencies in the United States, people find it hard to keep track of who is collecting which debt. Debts are bought and sold so many times that in the bankruptcy schedules we prepare we often list multiple debt collection agencies for one debt just toRead more

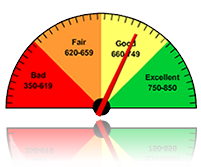

What Makes Up Your Credit Score?

Prospective clients often ask how their actions will impact their credit score. Much of what makes up the credit score is deliberately kept secret by the privately held corporation that developed credit scores. The three credit bureaus (Equifax, Experian, TransUnion) and individual creditors may also have different scores. Mainly, because they use a different credit score model or because not all creditors report to the same bureaus. But we know generally that the FICO score created by Fair Isaac is madeRead more

The Sallie Mae Empire

With over $1 trillion in debt, federal student loan debt now exceeds credit card debt and over $120 billion of that student loan debt is delinquent. A January 2014 report from the National Consumer Law Center (NCLC) called “ The Sallie Mae Saga: A Government-Created, Student Debt Fueled Profit Machine,” details the extensive role Sallie Mae plays in the student loan industry. What Is Sallie Mae? Sallie Mae was created in 1972 as a government-sponsored enterprise that could use publicRead more

Colorado Sues Debt Buyer

A lawsuit brought by the state of Colorado late last year sheds light on the world of buying charged-off consumer debt. What was the lawsuit about? In a lawsuit against several debt collectors and debt buyers, Colorado said the companies had purchased thousands of charged off debts from U.S. Bank and Wells Fargo for likely just pennies on the dollar. But even though the banks transferred the debts to the companies, no documents related to the debts were also transferred.Read more

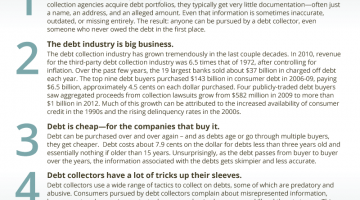

Escaping the Debt Machine

Over one billion contacts are made each year by debt collectors to consumers. The contingency fees raked in by third-party debt collectors exceeds many billions of dollars. The largest debt collector, NCO Financial which is owned by JPMorgan Chase, earns nearly $2 billion annually. A report describes both the enormous profits in the debt collection industry and the flaws in the legal system. Judges in Iowa estimate 85% to 90% of all collection lawsuits result in a default judgment becauseRead more

- « Previous Page

- 1

- …

- 9

- 10

- 11

- 12

- 13

- …

- 16

- Next Page »